How you draft a founder’s agreement can define the growth of a young company. Knowing what’s best for founders and the company before drafting this agreement becomes essential. Legal educator and international attorney Komal Shah deconstructs a generic founder’s agreement. Talking about the practical nuances, Komal says, these documents can either set healthy expectations or spark a conflict. This agreement is all about recognizing and incorporating the various elements in a startup that relate to the founder’s interaction.

Questions in this Episode

- In a founder’s agreement, how do ownership and vesting work?

- What are the fiduciary duties to consider when drafting a founder’s agreement?

- What is the significance of defining confidentiality and what should be included?

- How to draft a fair “resignation and removal of founders” clause?

- What can be done to make founder agreements more inclusive?

Why are Founder’s Agreements so Important?

With the startup industry booming throughout the world, it’s more important than ever for startup founders to function in harmony and avoid conflicts. Issues such as one founder outperforming the other or receiving more money for doing less work can arise, which is why it’s important to draft an agreement and record each founder’s compensation even before it’s incorporated. When drafting this agreement, it’s critical to discuss and negotiate issues like ownership, vesting, and duties. Let’s take a look at each one individually.

The ownership clause in a founder’s agreement becomes critical because people need to know what they're working for. - Komal Shah #ContractTeardown Click To Tweet

Ownership & Vesting in a Founder’s Agreement

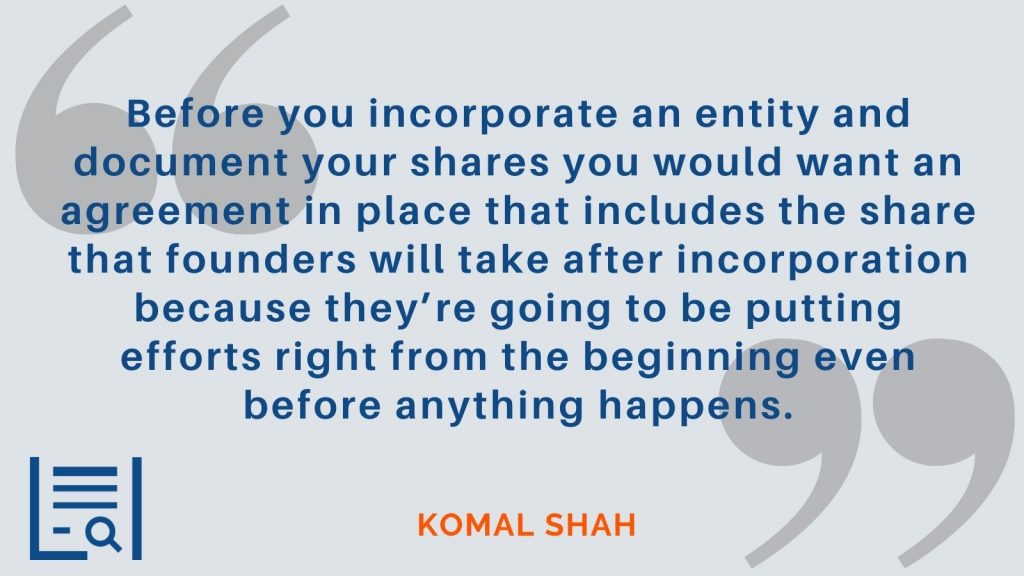

In the initial phases of the startup, there is no incorporated entity yet but you’re starting a business with the hope that you’re going get a good deal of return, your idea is going to take off and you’re going to make a truckload of money. Founders wish to know the ownership each of them is going to have because they’re working for it.

Someone can work for four hours and make a lot of sales, and someone else can work all day and have a hard time moving stuff, which is why getting at a highly objective mechanism of share in ownership is a bit tough.

Vesting is the process by which people begin to get their rights to the shares and the percentage of those rights. When the company is incorporated, it is easier to add the dates that have been allotted, however when the business is not incorporated, it becomes difficult because you don’t know when the shares will actually come into existence.

Fiduciary Duties: How Much is Too Much?

When drafting the fiduciary duties clause, keep these points in mind:

- Don’t benefit personally from the company’s operations.

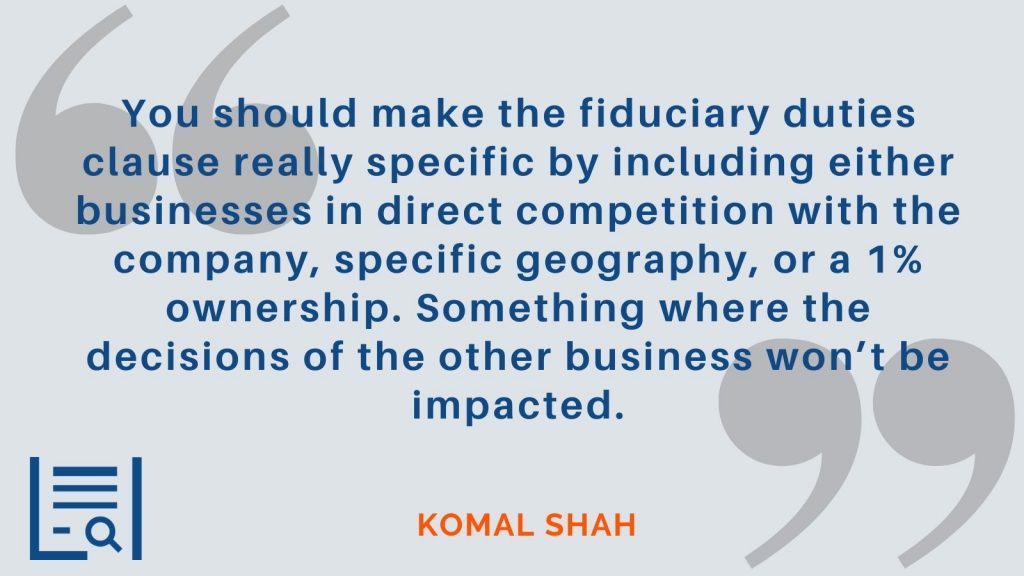

- Do not engage in any activity that is detrimental to the company’s interests, such as opening a shop in direct competition or something similar.

- Do not do anything that will benefit someone personally at the expense of the company as a whole.

| 9. | Fiduciary Duties |

| The Founders must refer to the Company, in writing, all opportunities to participate in a business or activity that is directly competitive with the Company within [GEOGRAPHIC REGION], whether as an employee, consultant, officer, director, advisor, investor, or partner. |

If you make the terms of holding shares or a percentage of other companies restrictive, the courts may not agree with you if you seek to fully prevent founders from investing in any competing business. Assume you’re preventing founders from starting businesses that are related to the company but not in direct competition, and you’re preventing them from doing so across all geographies. For courts to agree on something like that becomes incredibly broad and unreasonable.

Drafting a Confidentiality Clause

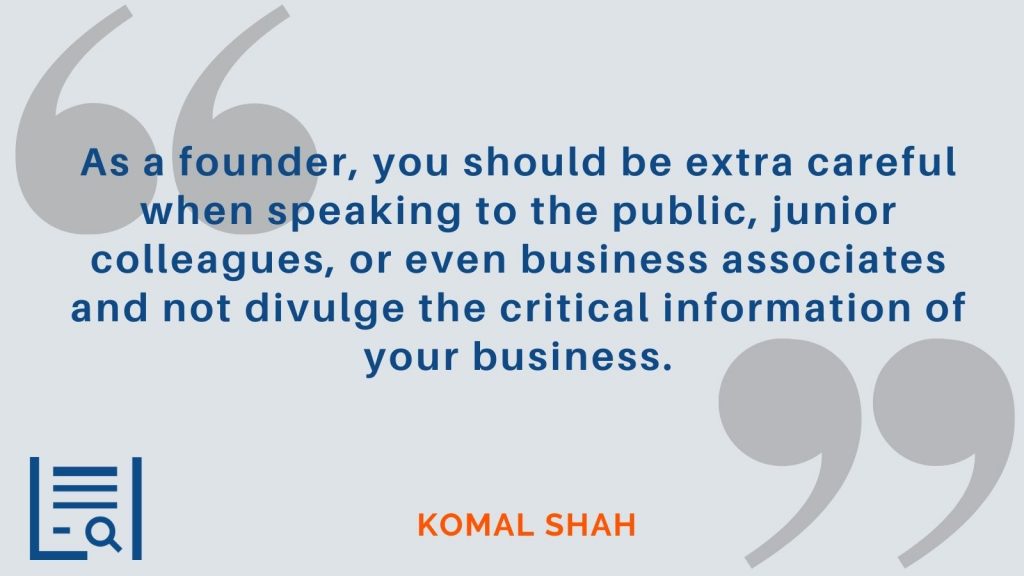

Make sure that the most important aspects of the business, such as the business model, specific processes, main customers, customer terms, product development plans, and so on, are kept as confidential as possible. How you define confidential information becomes important.

You don’t want to keep anything and everything confidential because it’s critical for a founder to get out and talk to other folks about their business. It’s all about finding the right balance. Confidentiality issues can create tensions between founders, resulting in failing founder relationships.

Ending the Relationship: Resignation and Removal

In section 11, the language used is mind-boggling. Saying that “majority of founders may remove another founder from the company at any time for any reason or no reason” or saying, “any founder may resign from the company by giving written notice” is too broad.

| 11. | Resignation and Removal of Founders |

| Any Founder may resign from the Company by giving written notice to the other Founders. A majority of Founders may remove a Founder from the Company at any time, for any reason or no reason at all, by giving written notice to such Founder. Upon a Founder’s resignation or removal, the Company will continue and will not dissolve, so long as at least one Founder remains as a member of the Company. The Company will pay out to the resigning or removed Founder his/her capital account balance (if any) within 180 days of resignation. |

It’s not a good idea to grant other founders a blanket right to remove any founder that way. It’s only fair that founders be given an opportunity to be heard and a specific period of notice. However, if the board of directors and majority votes are against the founder, that founder may not be able to continue for long.

Make it Inclusive and not Restrictive

This document’s social function can be summarised as “you want to pre-litigate so you don’t have to relitigate.” It’s as if you’re bringing drama into a relationship before it even exists.

Rather than one founder restricting the other from doing something, founder’s agreements seek to set expectations and a tone that displays passion for the business and a sense of involvement from all founders. This agreement should be reviewed after each key event in the startup, but it’s vital to remember that you shouldn’t rely on it for the entirety of the relationship.

Final Tips When Drafting a Founder’s Agreement

Define decisions that require universal approval from all founders, such as bringing in a third party, dissolving the company, investing in a new project, purchasing real estate, or hiring someone at a high level.

It’s a good idea to divide and segregate responsibilities when drafting a founder’s agreement. When one founder looks at marketing, another at finance, and another looks at sales, the agreement becomes much more clear.

Show Notes

THE CONTRACT: Generic Founder’s Agreement

THE GUEST: Komal Shah has over a decade of experience working in and leading in-house legal and compliance teams in large and small multinationals. Now she takes responsibility for compliance of subsidiaries across 19 countries. She is currently building a vertical as an intrapreneur and can be reached on LinkedIn, her email (komal@ipleaders.in), or on Twitter.

THE HOST: Mike Whelan is the author of Lawyer Forward: Finding Your Place in the Future of Law and host of the Lawyer Forward community. Learn more about his work for attorneys at www.lawyerforward.com.

If you are interested in being a guest on Contract Teardown, please email us at community@lawinsider.com.

Transcript

Komal Shah [00:00:00] That’s the reason why you have a Foundas agreement in place.

Intro Voice [00:00:02] Welcome to the Contract Teardown show from Law Insider, where legal experts tear down contracts from some of the most well-known companies and high-profile executives around the world.

Mike Whelan [00:00:17] In this episode, legal educator and international attorney Komal Shah tears down a generic founder’s agreement. As Komal says, these documents can either set healthy expectations or create a divisive fight. How you draft a founder’s agreement can define the growth of a young company, so let’s tear it down.

Mike Whelan [00:00:37] Hey, everybody, welcome back to the contract tear down show from Law Insider, I’m Mike Whelen. The purpose of this show is exactly what it sounds like. We take contracts. We beat them up. We are often mean, occasionally nice and supportive to our loving contracts, but not usually. Usually we’re pretty mean. Today, I’m here with my friend Komal Shah. Komal, how are you today?

Komal Shah [00:01:00] I’m great and excited to be here.

Mike Whelan [00:01:02] I’m excited. I mean, as excited as a person can get about contracts, right? I’m excited. We’re going to be talking about this document. This is a founder’s agreement and we’re using sort of a general version because these tend to be very private documents, but we’re going to go through this. Come on, why are we talking about this document? What’s important about it? When are lawyers are likely to see it. And why should they pay attention to this conversation about a founders agreement?

Komal Shah [00:01:28] Yeah, well, see if you if you look at the start up, see that’s exploding everywhere around the world and you would warn that the founders of a startup function in harmony and they don’t have conflicts and they don’t have issues down the road like, you know, you’re doing better than me or like, you know, he is getting more instead of putting in less work, this kind of issue is going to arise. So you want to put something in an agreement to get to get the contribution to the goal, the contribution to record what they’re going to get from the business down the line even before it’s incorporated and ensure that there are no conflicts. And that’s the reason why you have the founders agreement in place.

Mike Whelan [00:02:10] Well, we’re going to talk about sort of the social function of this thing and whether this document actually brings founders together or tears them apart. I might even make an analogy to a prenup and marriage, though probably not a great analogy. But before I do tell me about Tell us about you, Komal, what’s your background? What are you bringing to this document? Where are you seeing them?

Komal Shah [00:02:32] I’m a lawyer in the shadow secretary, and I’ve heard quite a lot of start ups get going. So like, help them through the way in all their incorporation requirements for admission requirements, their basic registrations, their basic contracts. I’ve helped them a lot of startups through this and I’ve seen that there can be issues which can arise later on between the founders if they don’t do something like an agreement. Basically, I work with Law School, which is a leading edtech in India and one of the co-founders of that startup. So I also kind of understand how the founders feel. Everyone is taught that they wanted to in growing a business, and that’s how like A. I believe I can work through founders agreements,

Mike Whelan [00:03:17] and I’ve been married for 20 years. And so, you know, I know exactly how this goes. Do the only ship that don’t sail is a partnership, as Dave Ramsey occassionally says. So we’re going to see if we can make this ship sail. Let’s go into the document, Komal starting at the ownership of the company. You wanted to talk about the shares in the way the shares are divided. You know, I’m assuming that when these companies are starting, there’s really not much to divide. So you’re sort of talking about an abstract. So tell me about how you think through this ownership of the company section. This is section five in the document.

Komal Shah [00:03:52] Yeah. So what happens in the beginning is that you don’t actually have an incorporated entity it, but you’re starting a business with the belief that you’re going to get a good deal of return. Your idea is going to take off and it will make a truckload of money. That’s how you start off. But then before you incorporate an entity and actually get to documentos your shares and everything, you would want an agreement in place on what is going to be the share that someone would take once the company gets incorporated. Because you’re going to be putting effluent right in the beginning, even before anything happens, you’re going to start putting the effort. You’ll be able to start arranging things so people want to know what is going to be the return for which they’re working. And that’s the reason why the share or what is the ownership of the founder each of the founders is going to have is very, very important. It’s more important because it’s very difficult also to determine that X will have X number of shares because he’s putting X number of hours or it is contributing X number of things because someone can be putting in four hours and generating, you know, a lot of sales and someone can be working for the whole day and make it find it very difficult to move something. So that’s why, you know, arriving at a very objective mechanism of share in the ownership is a little bit difficult. People use different tools for this like, you know, founders by calculator and all of that and assign later to do the kind of work for hours or the results generated. And that’s how they decide to shares. But that’s why this class becomes critical because people need to know what they’re working for.

Mike Whelan [00:05:32] Hey, everybody, I’m Mike Whelen. I hope you’re enjoying this episode of the contract teardown show. Real quick, I want to ask you to do me slash you really a quick favor. Look down below. You’ll see a discount code to join the Law Insider Premium subscription. When you do that, you get access to more content like this. You’ll see webinars daily tips on contract drafting, not to mention access to the world’s largest database of sample contracts and clauses. It will help you write better contracts faster if you want to do it. Right now, there’s a code below, so get there. Also, if you’re part of a larger team, if you’re in-house or in a law firm, just email us where it’s sales@lawinsider.com will make sure you get a deal as well. Come join us in the community. The code is below. Let’s get back to the show.

Mike Whelan [00:06:18] Yeah, I wonder if there’s any way to do this again. I’m thinking of my own partnership experience, including my marriage. And, you know, at the beginning of the marriage, you think we’re going to have date night every week and our kids are never going to be the kinds of kids who scream in the store, right? It’s all this sort of sunny. But then when you’re asked to sit down and do the math of like, what’s the relative contribution that can be quite freighted? Thinking about six vesting? Talk to me about how the vesting happens and what the relationship is with that stock division in five. Talk to me about section six.

Komal Shah [00:06:52] Yeah. So Section six, if you look at the listing schedule or when people actually start to get the rights to the shares, it’s very important on what is the timing that you are entering into a founder’s agreement because all the founders agreements usually tend to be entered into before and incorporated entity comes into place. You can also have it after the incorporated entity is in place just as a measure of internal understanding between the founders because you have your constitution documents of the company, but that talks about the functioning or the mechanism or the relationship between the company and the share. Really does, while this is something that talks about the relationship between the founders, so you can also have it when it’s incorporated and then you do it afterwards, incorporated western is a little bit easy because you going to put like, you know, from the date when you have been allotted this year as its X date, you know this much period of time of year or two years down the line is when you’re going to have all the rights to the shares is a little bit difficult when you’re doing it without the entity in place because you don’t know when the shares are actually going to come into existence. So you either might want to bring it a little bit later when the company is formed, or you might want to divide the dates as the date from which the shares get allotted. Right. So that’s something that you want to put in. Listing West is basically when you get all the rights to the shares, that’s it and the percentage of rights.

Mike Whelan [00:08:21] Well, and there’s a section below about what happens if the if you know the agreement gets broken up or founder gets terminated in some way, what happens to the shares? Talk to us about that. That terminated founder shares section.

Komal Shah [00:08:36] Yeah, so if if a founder has shares and you know, they they get terminated because. And interestingly, I’ve had loads of discussions with startup founders on how are you going to try to share or, you know, you can buy a founder, you can not let them participate in the management decisions. But how are you going to fire a shareholder? It’s very difficult to fire them. So either you can buy back their shares if the law of the place allows you to buy back the shares, or you can kind of mandate them to transfer it to somebody else. OK, so when they cease to be a founder, they must transfer visions to someone else. Or if you know the whole lot of them is transferring their shares to an investor, then there’s a drag along right? And they would have to transmit to an investor something like that. So that’s how you get the shares back into the fold from the person who’s dominating the relationship. Mm hmm.

Mike Whelan [00:09:28] Yeah, I mean, I was thinking about this. It talks about a majority vote of the founders. And I assume usually when this kind of document is created, there’s only two, right? But it seems to really be targeted to the time at which the company is farther down the road, right? Like they’ve they’ve got investors, no more shares that have been assigned at that point. And so that kind of sentence probably makes more sense, then a little less sense early. Yeah. In down to seven and the management, right again, this is one of the major decisions with an agreement like this. How are you thinking about Section seven and the management rights?

Komal Shah [00:10:05] So there are certain decisions that you want to put in the business of the company, which should be taken ideally with a consent or with the agreement, all of all of the founders now, for example, you are going to talk of raising capital. You want to bring in the third party. You want to have the consent of all the founders. So you might want to divine certain decisions where it’s essential that both the all the founders and the Daryanani must be agreed towards it. You can also define decisions which will be taken by a majority of the founders, so decisions which are really, really, really, really critical to the existence of the company. Someone wants to dissolve the company or things like that would be critical to the business. You want to take that with the unanimous consent of all the founders. When you’re talking off decisions which are a part of the business, you know they’re going to support. Let’s say you want to make investment into some projects or you’re going to buy some property or you’re not to employ or hire someone at a very high level something like that. Those decisions you can put as something where a majority of the founders should agree, but decisions which are business political, you can vote as unanimous decisions. You might also want to divide or segregate the responsibilities. One of the voters will look at marketing and then there is a finance guy, and then there is a hardcore sales guy. You might want to divide that in your agreement. Also, just for clarity sake.

Mike Whelan [00:11:33] Yeah, I was thinking about like Section eight talks about identifying the different founder responsibilities because otherwise you’re going to end up with seven. You know, a majority of founders are due to take out the trash, right? But to divide the responsibility is gives you some space to to sort of section out the kinds of decisions and assign some gravity to those decisions, which makes sense. Jump down to nine to fiduciary duties. Talk to me about how the founders have, you know, assign these fiduciary duties to each other.

Komal Shah [00:12:04] Yeah. So what happens here is that, you know, it’s you. The basic fiduciary duty element in these things is that, you know, you wouldn’t want to profit personally from the functioning of the business. That’s just one thing that’s very relevant you wouldn’t want to do or you wouldn’t want to carry on the activity bodies which are against the interests of the business. Like you come out of the business and set up shop, which is in a direct competition with the business, that’s something that’s going to be impacted, right? So basic duties would be like a not carrying out a direct business which is in direct competition without the consent of the founders not trying to do anything that will give them give somebody a personal gain as against, you know, a guide to the business as a whole. So these are just basically some fiduciary points or elements of the duties of the founders, right?

Mike Whelan [00:12:59] Yeah. But you see a little bit below a bit of clarification on, you know, if somebody owns a mutual fund or something. And so they’ve got a very small chunk of ownership of a competing company. There’s a line that says the ownership of one percent or less of the securities of any publicly traded company will not be considered participation in a competitive business or activity. Do you think this is enough to clarify what participation means or should they add more to clarify that point?

Komal Shah [00:13:29] You can you can see you can define this how you want it. You want to make it a very restrictive condition or restrictive terms. Sometimes courts will not agree with that if you want to ban them completely from investing in any kind of competing business. And let’s say you are stopping them from doing businesses which are even related to the business and not exactly direct competition, and you are restricting them from doing it in all geographies. So that’s something that’s very wide and all reasonable. That’s not going to work. You want to make it really specific losing businesses which are in direct competition with a company or a specific geography or or, you know, which is in this business itself. So ownership of like, you know, companies one percent is something that you’re not going to be able to impact the decisions of the other business, but you might want to put that that, you know, you shouldn’t be able to impact or influence the decisions of that specific business, whether it’s by one percent ownership, whether it’s by being the director or the board board, or whether it’s being by a really influential consultant. In whatever ways, you don’t want to be in a position where you’re really able to influence and drive a competent competing business. So there’s the element. So you might want to extend this actually to a situation where someone is a director or someone is a really influential consultant.

Mike Whelan [00:14:51] Yeah, I don’t think anybody is worried that the CEO of Disney is going to call me and ask my opinion to, you know, hurt my own company for my tiny shares in the Disney Corporation. Let’s jump down to this bit about confidentiality clauses. How are you dealing with company IP and those kinds of sharing information from inside of the company? What do you want to see? What do you and don’t you see in this document?

Komal Shah [00:15:22] I would want to ensure that definitely elements which are very crucial to the business, like the business model of specific processes, product development plans, these kinds of things are kept very, very confidential. Now you want to be very careful even when you are speaking to the public, even when you are speaking to some of the junior colleagues, even when you are speaking, do you know, let’s say, your business associates that you don’t divulge this information, which is really, really, really critical, like, you know, business models or product development plans or major customers of the terms of its customers, things like this are very, very crucial. So it’s important how you define confidential information in in the agreement. You don’t want to make anything and everything confidential because in fact, for a founder, it’s a little bit essential that they go and talk about their business to different people, but elements which can actually result in a damage to the business, like a business model or an impending of plan or customer list or terms with customers. These things you don’t want to divulge at any place.

Mike Whelan [00:16:33] Yeah, jumping down to 11, it talks about the resignation of removal of founders, and I just got to read this sentence because it’s fantastic. Any founder may resign from the company by giving written notice to the other founders, and here’s a sentence a majority of founders may remove another founder from the company at any time for any reason or no reason at all by giving written notice to such founder. Obviously, when you’ve got two founders right, you know you can’t have a majority. There’s no it’s 50 50, but you know, you can see you get a love triangle of a third person into this company. And real quick, the drama gets really reality TV really fast. What do you think about the language in this resignation or removal section?

Komal Shah [00:17:17] I do not think that you can you should give a blanket blanket, right, do you know the other founders just to remove the founder just like that because it may happen that actually the wealth game gets together and removes the hero out of like A.. And they are driving the business after that just for their own benefit. Like, you know, you don’t want to do that. So you want to ensure that at least an adequate opportunity is given to any founder to to be heard. Do the other founders and then their views are actually documented, like that’s that’s no more fair. And it’s like just natural justice that you give someone an opportunity to to explain themselves and to want to put down their views into that document. Having said that, if it’s a board of directors and a majority votes against you, you’re going to have you, you’re going to get it out. It’s going to be very difficult even for the person to function afterwards. If the if the feeling of the rest of the people is that they don’t want to cooperate and you know, this person is the leader of the lot, then it becomes very difficult for that person, even if he stays to form to function. But definitely there should be an opportunity that’s given. And you also give a specific needed of note, as you can just say, you know, just like, you know, here it is, it’s delivered to you and you’re out. Like you can say right now you’re out it.

Mike Whelan [00:18:39] Yeah, yeah, yeah. No, well, I mean, you know, thinking big picture, you look at this document, it’s only five pages, right? So, you know, with this kind of relationship, this is sort of more laying out principles than it is trying to imagine every possible. And so I’m thinking about the social function of a document like this in, you know, when I did mediations and in business and in family law, what I would always say is you want to pre litigate so you don’t have to relitigate. So let’s decide this stuff now so you don’t fight it out in court later. And that’s sort of a function of a document like this is let’s think about the future. But of course, as soon as you start pre litigating, you’re like introducing drama into the relationship before it was even there. So thinking about this document, do you how do you as a lawyer, as a practicing lawyer trying to get this relationship consummated through this document? How do you use this document as a way to strengthen the relationship as opposed to kill it before it starts?

Komal Shah [00:19:38] Yeah. So basically, these founders agreements also also work on setting the expectations and setting the tone that, you know, this is what we agree up. We’ll dedicate ourselves to the business. It’s not like, you know, someone has to stop us from going out and doing that. We’ll do that. We’ll give our IP, we’ll give those real contributors. That’s the sense of the document rather than, you know, two or three of them stopping the other person from doing that, that it sets the expectation right at the beginning because, you know, it’s a joint agreement people are agreeing to do to bring a business end to scale it and to profit from it, right? So that’s how you do it. And when you’re doing it, you want to ensure that when you’re setting it, when you’re putting it, you want to end your terms. You want to ensure to put warnings which are not really restrictive and which no sound like, Hey, I’m making you do this rather than, you know, let’s do this. That should be the tone of the document. You want to use language like this that let’s have that OK, so that it’s the language of language or the enrollment that you want to set, whether you’re putting or drafting the document.

Mike Whelan [00:20:47] Yeah, I it’s again the bad analogy I’m thinking of. I remember talking to a lawyer about a prenup, about prenuptial agreements and what he advised his clients was revisit this after every major life event, right? So don’t try to rely on this document for the entirety of your relationship revisit. And so for a document like this, I’m thinking this is pretty bare bones. And yes, it’s set some expectations, which is important because you know what harm is a breach of expectations. And so by making them clear, you can define those are. But you know, also this is pretty slim. And you know, it’s obviously a document that you your company’s worth jackal when you start, right, it’s not worth anything. But yeah, go on. Things are going to happen. Revisit these kinds of agreements as you go on. I think it’s really smart. Just get the company moving and you can dig into the drama later. So for people who want to reach out to you? Komal, I appreciate you running through this for people who want to reach out to you. Learn more about what you do about your learning company. What’s the best way to connect with you?

Komal Shah [00:21:53] The best way to reach me is my email I.D., which is komal@ipleaders.in, I can leave it with you and that’s that’s the best I have. Like, I want that all the way. Yeah, that’s that’s sad, you know? You can also reach out to me on LinkedIn, I’m there on LinkedIn as well. You can reach out to me on LinkedIn, on Twitter. Also, I’m there, so good of there. Most of those platforms I love, they’re underrated too. But like, you know, LinkedIn and email, it is where I regularly. I’m regularly there as well.

Mike Whelan [00:22:27] We’ll share that information at at the blog post, at LawInsider.com/Resources, where we will post this video and all of Komal’s information. Also, if you want to be a guest on the contract teardown show, just email us at Community@lawinsider.com. We would be happy to have you. Thank you, Komal. Thank you all for watching. We’ll see you guys on the next contract teardown show. Have a good day.

Komal Shah [00:22:50] Thank you, Mike, and thanks, everybody.