When a business sells shares, there’s an interesting space between when a deal is agreed upon and when it finally goes through. In that time, there can be significant changes in working capital and the overall valuation of the business.

In order to account for any differences, the purchase agreement includes multiple provisions to ensure detailed and accurate accounting. What follows is an analysis of the purchase price mechanisms in a 1997 Stock Purchase Agreement from Global Imaging Systems, a sales and service company for manual typewriters.

This historical deep dive covers a carefully planned transition to avoid disputes over the final purchase price. Consider what we can learn from looking at this contract, which was written in an era where capital was flowing and share sales were happening in abundance—just like today.

Questions in this Episode:

- How is a 1997 agreement relevant today?

- Why use working capital as a main metric?

- What happens when the working capital target is missed?

- How is the price adjusted after closing?

- How are today’s agreements different?

The Relevance of a 25-Year-Old Agreement

This teardown reviews a 1997 stock purchase agreement between Global Imaging Systems, Electronic Systems Inc., and others. Global Imaging Systems began in 1956 as a sales and service company for manual typewriters. It evolved into a document solutions company and was acquired by Xerox in 2007 for $1.5 billion.

What’s remarkable about this 25-year-old agreement is that the core principles of stock purchase agreements are still the same.

The parties typically establish the purchase price based on the company’s value. But there are often several months between making the agreement and the closing, during which time the company might increase or decrease in value. So the parties establish a purchase price adjustment mechanism to account for the inevitable change in the company’s value.

For example, if the company is valued at $10 million at the signing of the purchase agreement but only worth $9 million at closing, what mechanism is used to adjust the purchase price? What numbers, metrics, and accounting methods do the parties use to adjust for the company value at closing or even after closing?

One of the metrics used by this contract is working capital, which in simple terms is the money that a business needs to support itself as a going concern.

The seller provides an estimate of what the balance sheet looks like at closing, and there are adjustments for working capital and purchase price. And after closing, the buyer provides a closing balance sheet and typically does an audit 120 days after the closing. That is when the final adjustment occurs.

Preliminary Closing Balance Sheet

The formatting of this agreement puts four pages of definitions at the top of the 34-page document. It explains terms like Preliminary Closing Balance Sheet, Working Capital Target, Working Capital Adjustment, Funded Indebtedness, and more.

The Preliminary Closing Balance Sheet is defined as the Company’s best estimate of the Company’s balance sheet as of June 30, 1997. And the seller must deliver the Preliminary Closing Balance Sheet to the buyer no less than one or more than five days before closing.

So when the buyer receives the balance sheet, they compare the working capital on the balance sheet to the target working capital. Even at this stage, if there is a difference, they can make an adjustment.

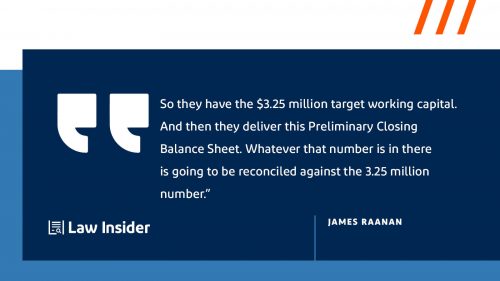

For example, if the target working capital was $3 million, but the working capital on the Preliminary Closing Balance Sheet was only $2.5 million, then the buyer will reduce the purchase prices by the difference between the two; in this example, $500,000.

But the simplified definitions of the older agreements can lead to issues. This agreement does not define which accounting principles will be used, and that can be significant with items like bad debts. Some companies write off bad debts after 90 days, and some run them up to six months before writing them off. Depending on which write-off dates are used, the parties may disagree on how the receivables should be reflected on the balance sheet.

And this confusion could lead to an overstatement in the working capital because working capital includes receivables minus current liabilities.

Working Capital Target

“Working Capital Target” is explicitly defined in this agreement as $3,325,000 minus the Working Capital Adjustment.

And “Working Capital Adjustment” is defined as an amount equal to $80,548.

Using specific amounts is a foundational assumption. But it is quite common in these types of agreements because it provides an amount of certainty. But the bigger question is, how did they arrive at those numbers, and are they accurate?

For example, when determining working capital, what kind of averages are they using, and are they including or excluding seasonality? Many industries, like entertainment, have significant seasonal swings in revenue. So there are often more receivables around the holidays than during the rest of the year. And this impacts the calculation of working capital.

Funding Indebtedness

Funded Indebtedness deals with certain debts and obligations of the Company, like debts for borrowed money, obligations for deferred purchases, capital leases, accounts payable, accrued expenses, and more.

In this agreement, it appears that the buyer is trying to exclude longer-term debt. Typically, that is something you often see in agreements like this as an adjustment for cash and debt, which is then an adjustment to working capital.

But here, the agreement states that the buyers can pay down the debt, and that amount will come off the purchase price.

But some issues are not addressed, like prepayment penalties. What happens when the buyer pays down debt but has a prepayment penalty because they are paying the debt too early? It’s hard to know what the drafters were thinking 25 years ago or why they wrote it that way. But this ambiguity could cause a problem.

Purchase Price Adjustment

The purchase price can be adjusted depending on how accurate the working capital target is since this is one of the main metrics on which the deal and purchase price are based. If this amount is off, the price is adjusted according to the terms of the Purchase Price Adjustment clause at 2.6.

First, the purchase price is reduced by the amount of funded indebtedness. Then, the portion of the purchase price payable at closing is adjusted by the difference between the working capital stated on the Preliminary Closing Balance Sheet and the Working Capital Target.

And the adjustment can go up or down depending upon if the difference is positive or negative.

Closing Audit

Within 120 days following the closing date, the seller must deliver an Audited Closing Balance Sheet to Global. And this agreement calls explicitly for the accounting firm Ernst & Young to prepare that audit.

The seller prepares the first balance sheet, and at that point, the buyer should have a good understanding of the business, and there should not be too many surprises.

The after-closing audit is typical in these types of agreements. Then the buyer takes control and prepares a closing balance sheet. The Post-Closing Balance Sheet, as of the closing date, is compared to the Preliminary Closing Balance Sheet, and the two are reconciled.

If the seller disagrees with the final amount and wants to challenge it, they must pay for an independent audit. If the audit shows an increase of more than $125,000 in the Company’s working capital, then Global will reimburse the costs of the audit. Otherwise, the seller is stuck with paying for the audit, which can easily cost more than $125,000.

Post-Closing Purchase Price Adjustment

The final and ultimate price adjustment comes down to the Post-Closing Purchase Price Adjustment. And although this section is relatively straightforward, its lack of detail does raise some potential issues.

This section states that the purchase price will be adjusted up or down on a dollar-for-dollar basis on the difference between the working capital, as reflected on the Audited Closing Balance Sheet, and the Working Capital Target.

Seems simple enough. But the section is silent on what type of accounting to use, other than to state working capital should be calculated according to GAAP, generally accepted accounting principles. And this section does not go into any detail about the accounting principles used in the Preliminary Closing Balance Sheet.

This lack of detail may cause a mismatch in the calculations, procedures, and other expectations between the parties.

For example, the seller has only ten days to dispute the figures. That is an extremely short time window for such a complicated transaction. And if the sellers do not object, then the money is paid out according to the final undisputed terms. In more modern contracts, typically, you would see 30 to 60 days as a more common dispute window.

And there are also more nuanced potential issues.

For example, the Audited Closing Balance Sheet shall be done by Ernst & Young. And if the seller objects, they must use one of the “Big Six” accounting firms, which are now down to the “Big Four.” And it states that the parties shall choose this arbiter accountant jointly. But what if the parties do not agree? What then? How is this resolved? It would be better to draft a more tightly defined procedure.

The problem is not so much with this section because I think it is pretty clear. The issue is within the definitions that underlie it. - James Raanan #ContractTeardown Click To Tweet

Then and Now – Evolving Differences

So what are the significant changes in these types of agreements since 1997?

There are two.

First, the main difference in the drafting is the added detail in more current documents. This stock purchase agreement is about 35 pages, whereas today, it would be about 70. This added detail removes many of the issues and ambiguities caused by the simplified and less detailed early types of agreements. Today’s contracts are more balanced.

The other change is in the marketplace. Over the past few years, there has been the availability of capital. And this means that money is chasing these types of transactions instead of the transaction searching for funds. This is reflected in the drafting and the resolution of these agreements. As a result, many of the resolutions are more toward the seller’s side. Because there are more buyers and capital out there if the transaction does not go through, the sellers currently enjoy an advantage.

Show Notes

Stock Purchase Agreements cover complicated business transactions that can take months to close. These contracts include purchase price mechanisms to account for when the business’s value might change between the execution date and the closing date. In this episode, attorney James Raanan tears down Global Imaging Systems’ Stock Purchase Agreement and shows the evolving use of purchase price mechanisms to account for changing business valuations.

THE CONTRACT: Global Imaging Systems Inc Article II Agreement of Purchase and Sale Closing

THE GUEST: James Raanan is an international corporate and commercial lawyer, with both substantial in-house and private practice experience. He is especially active in the telecom and fintech spaces. He lives in Israel, practiced in the US and was raised in England. He has recently joined the Israeli firm of Amit Polak Matalon – as a partner in their technology and VC practice, as well as head of telecom.

THE HOST: Mike Whelan is the author of Lawyer Forward: Finding Your Place in the Future of Law and host of the Lawyer Forward community. Learn more about his work for attorneys at www.lawyerforward.com.

If you are interested in being a guest on Contract Teardown, please email us at community@lawinsider.com.

Interview Transcript

Mike Whelan Hey, everybody welcome back to The Contract Teardown Show from Law Insider. I’m Mike Whelan. The purpose in the show is exactly what it sounds like. We take contracts, we beat them up, we’re mean to them, occasionally nice, but that’s rare. We hang out with smart friends like my returning buddy, James Raanan. James, how are you today?

James Raanan I’m great. It’s great to be back.

Mike Whelan I am excited to talk about this one. The thing I like about you as you bring me the nerdiest, like, you really get into these like complex bank deals, which is fun because it’s a level of nerd that, you know, I just don’t understand. So I get to ask the dumb questions. Let’s start with what this document is. I’m going to share it with people. This is a Stock Purchase Agreement By and Among Global Imaging Systems, etc. We’ll share the link below and over at the blog at Law Insider dot com slash resources. But we’re going to focus on this section. Before we do that, James, tell me: What is this document? When are we going to run into this kind of thing?

James Raanan So this is a share purchase agreement or stock purchase agreement. And the interesting piece of this agreement that I really want to focus on is the purchase price mechanism, which helps the party—when they agree in the original commercial negotiations, there’s a time lapse right between when you agree on something, when you finally do the deal. And in between those two dates, the business could reduce or increase in value. And how do you solve for that?

Mike Whelan Hmm. Interesting. Yeah, and we’ll do that. We’re going to focus…this is all down in section—Article II. Really focus starting in 2.6., so we’ll get down to that. But before we do that, we’re going to talk some definitions. But prior to that, let me ask about you. Remind us, James, what’s your background? How do you come to documents like this?

James Raanan So I’ve been doing this now for 26 years, and as you said, I’m a little bit nerdy about these things. I actually find this absolutely fascinating. I don’t know what that says about me. I’m originally from the U.K., went to law school in the U.K., then came to Israel and participated in the dotcom boom as a lawyer. So I did many, many deals and cut my teeth when I didn’t know anything. Then the later clients got the benefit of all of that experience. And today, I have my own practice after having been the GC of a large U.S. telecoms company. And I really focus on deals, typically M&A or investment deals for family offices, family businesses who are being bought or buying other companies. And then sometimes, I just act as a consigliere to the much larger corporations working with other outside counsel. So we come across this kind of stuff a lot, and as I said, I find it pretty fascinating.

Mike Whelan Perfect. All right. Cool. So what we’re going to do, as you mentioned, we’re going to start with the definitions in here. This document does do the thing where the definitions are set out at the top, rather than being contextual. And so there’s a bunch of terms that are up top that will come up later in section two when we’re talking about adjusting the purchase price. So let’s roll down to that. I’m going to go just alphabetically, as this does, to Funded Indebtedness. It talks about—it’s all the indebtedness of the company for borrowed money, etc. What do you think about this definition? It’s got a long list of things that could be funded indebtedness. What do you think about this list? Is it exhaustive? Do you like it?

James Raanan So this is a very interesting definition and in some ways quite old-fashioned. And maybe let me use that as a segue to kind of give you a little bit of an introduction to this agreement, to give a bit of background. And it’s quite interesting. This agreement is from 1997. And what’s remarkable about this agreement is in many ways, the core concepts haven’t changed since then, but there’s a lot more detail you see in modern day, right? This is over 20, almost 25 years ago, M&A agreements, this agreement was with a company who was at the forefront of developing typewriters and keyboards. They were bought by another company, which was then bought by Xerox. The original company I think was bought for $400,000. And then in this transaction, it doesn’t say how much it was sold for, but for substantially more. So it’s just interesting to see how things have developed. And just, sort of, to give you a background before we get into the definitions, as I said before, when you initially establish an agreement on the value of a company, there’s usually several months that run between then and between you signing the agreement. And so what you try and set up is a—often set up—is a purchase price adjustment mechanism. So if you agree that the business is worth $10 million, you want to check at the closing or after the closing, that in fact, that’s how much the business is worth. And so you agree to adjust the price based on movements that can happen in some of the financial metrics of the business. And what this particular purchase price mechanism focuses on is an adjustment for working capital, right? So working capital in very simple terms is the money that a business needs in order to support itself as a going concern. And the way they have set up this mechanism of this agreement is that they, the sellers, provide an estimate of what the balance sheet of the business looks like at the closing that adjusts the working capital target and the purchase price. And then after the closing, and we’ll get into this later, the buyers then provide what’s called a closing sheet balance, then do an audit, effectively, 120 days after the closing to really see, at that closing date, what was the balance sheet to the company, to check whether what they received was accurate or not. We’ll get into how the adjustment works, but it’s important to understand that they’ve approached it in this two-step way. So getting to the definition you are speaking about—

Mike Whelan Well, actually, let me jump you down, because I want to come back to the debt, because to your point, you know, rather than just going alphabetically, let’s look at the next one that you’ve highlighted, which is Preliminary Closing Balance Sheet, because I think, if I’ve understood that right, what you just said, that is the mechanism that is trying to go back and figure out what the debts are, figure out what capital is is on hand and balance that out. So let’s jump down to that term, preliminary closing balance sheet. What do you think about that one? Why is it in here, to the mechanism that you were talking about?

James Raanan So the way that the agreement sets up is that it says here, not less than one, nor more than five days prior to the closing, this preliminary closing balance sheet is delivered to the buyers. And so the buyer receives that balance sheet and then it compares the balance sheet working capital to what they call the target working capital. In this agreement, they agreed on what’s called, let’s say, a target working capital, which is something like $3 million and change. And so even at that stage, to the extent that there’s a difference, then they’ll make an adjustment. If the working capital in the preliminary closing balance sheet was two and a half million dollars, then they will reduce the purchase price by the difference between that amount and the $3 million target working capital, because that means the business doesn’t have enough working capital to fund itself, and that means then the buyer has to put that money in. So one of the interesting things in going back to the history of agreements is this is a very simplified definition. It doesn’t talk about the accounting principles that are going to be used, and that can be really important because if you think of something like bad debts. So some companies will write off bad debt after 90 days. So they’ll remove that from their receivables. Some companies will run them for 120 days, six months. And so when they reflect those receivables in their balance sheet, there’s a big difference. What they don’t get into here is specifying the principles that are going to be used for…well, really any accounting principles. But I just use bad debt as an example. And what that means in terms of the ramifications as a buyer is that that could lead to an overstatement in the working capital, because working capital is my recei—my current assets, which includes receivables, minus my current liabilities. So if I don’t calculate bad debt properly, or if I overcompensate for bad debt, then I’m overstating the quality of the receivables in the balance sheet.

Mike Whelan Well, let me ask you, you know, down and again, working down to the definitions, you mentioned this working capital target, and they put even in the definitions a very explicit number. They say, “means an amount equal to 3.325 million, minus the working capital adjustment,” which is what we’re talking about in this, is how you adjust it. Is that normal in this kind of document to say—I assume they pick this number because they’ve put some kind of offer on the table and the offer, this is them solidifying that assumption on paper. We made that offer on the assumption that this is what you had, and if that’s not true…. Is that normal? To put a specific number like this in the definitions as sort of a foundational assumption like this.

James Raanan You know, you see it quite a lot. And I think the—it’s quite a—the nice thing about it is it provides some amount of certainty. The more interesting part of it is, how do they get the number right? So in the process of their due diligence, they have to have their accountants calculate what is working capital. So they could look at the last balance sheet they got. But you want to try and take some kind of average over the year, because there’s sometimes seasonality, right? If you’re in the…I don’t know, if you’re in the entertainment business, then there’s going to be seasonality. You know, often around the holiday period, there’s going to be seasonality. So you’re going to see a lot more receivables in the holiday period than you would do in January. So how you calculate it is actually really interesting. But yeah, you do see it quite a lot. You sometimes see, you know, something a little bit more vague which gives some benefit to the—well, really to the buyer sometimes, if they want to make a case that the working capital should be higher, but it’s much easier to have a specific number.

Mike Whelan That’s interesting. I was reading one of Geoffrey Moore’s books about shifting from sort of the start-up period to the established business period. And he talks about one of the things that you see is instead of the hockey stick money situation, you start to see the cyclical money situation. And so, you know, if you’re offering on a business that’s in that hockey stick, you gotta realize eventually you’re going to get to this, so it’s interesting. To your point, it does mention in the definitions, both working capital and as we talked about before, the funded indebtedness. The working capital, it says, is the difference between the company’s current assets and its current liabilities. And then it talks back in the definition about funded indebtedness and what can be included in that. Reverting back to that, do you like this list? Do you think this is an all-inclusive way to view funded indebtedness? Or to your point, do different companies have different views of what debt even is that matters?

James Raanan So it gets pretty technical because the purpose of them creating the funded indebtedness definition, I think, right—you can’t ask these people and this was 24 years ago, so who knows?—but I think they’re trying to exclude what is classically debt or longer-term debt, because that’s very often—sometimes you’ll see, in agreements like this, an adjustment for cash and debt and an adjustment for working capital. I think they’re deliberately treating longer-term debt differently here, because they say that the buyers can pay down this debt and then any amount that they pay down comes off the purchase price. What I think that they, you know, again, going back to the more laconic nature of an agreement like this in 1997 is that there are certain things they don’t include in there. So, for example, prepayment penalties, right? So they have to pay, you know, so they’re going to pay the debt. But what if they have to pay a prepayment penalty because they’re paying the debt too early? So they got to pay like the interest that the bank would have received during that period or whatever other penalty, etc. I mean, I think it’s reasonably decent and I think maybe, you know, sometimes as lawyers nowadays we kind of over-lawyer things. From the searches I did, there didn’t seem to be any litigation on this contract. So maybe it’s a lesson to all of us that drafting things more simply is the way to go.

Mike Whelan Oh gosh, it reminds me of a conversation I had with Sarah Fox where she said something like only 1.5% of all contracts are even litigated. And so obviously there is a question of do you pre-litigate through contract-drafting well, so you don’t have to re-litigate later, which actually brings us down to 2.6. It talks about the purchase price adjustments. So let’s jump down to that and see, did they lay good groundwork to avoid fights later? In B, it talks about “the portion of the purchase price payable at closing will be reduced by the amount, if any, by which the adjusted working capital,” which we talked about, “as reflected on the preliminary closing balance sheet, is less than the working capital target.” So again, just laying it out so I can totally understand this, the working capital target, correct me if I’m wrong, was the amount that they said, this is what we think the deal will be based on. So this is our number. Then they do an accounting, which is the preliminary closing balance sheet. And then as we’ll talk about later, they do a second accounting. Is this adjustment referring to the difference between target that motivated the deal and that first accounting? Is that what the section is talking about?

James Raanan Yes, you’re hired! Perfect. [Both laugh.] Exactly. So they have their 3.25 million target working capital, and then they deliver this preliminary closing balance sheet. Whatever that number is in there, is going to be reconciled against the 3.25 million number. So if it’s more than that, it can be adjusted upwards. If it’s less than that, can be adjusted downwards.

Mike Whelan And that accounting is seller, right? Because the next section talks about 2.7, which is the closing audit, which—talk to me about what that thing is, because I think that’s on the other side, right? That’s—they do a first offer, the preliminary closing balance, time passes, as you mentioned, closing audit. Correct me if I’m wrong. Is that what the closing audit is? And what’s the significance of that number?

James Raanan Yeah, exactly. So you’re absolutely correct. The seller prepares the first balance sheet because it’s the only one that can, really, even though at that point the buyer will have a very good understanding of the business and there shouldn’t be many surprises. Then after the closing in this agreement, the—and this is typical, really—the buyer takes control over preparing what’s called the closing balance sheet. So it’s accountants, or it takes accountants, usually typically with the company’s finance department, which then becomes its company. So it’s an interesting dynamic, right, for the CFO who before the deal closed, had one master. After the deal closed, has another master. So that’s always an interesting dynamic. But yeah, they prepare this post-closing balance sheet as of the closing date and then compare it to the preliminary closing balance sheet and reconcile the two.

Mike Whelan Yeah, there’s an interesting thing in here. They talk about the preliminary closing balance sheet being audited by Ernst & Young, and then they say if seller has a problem with it, then you can go back and they specifically say you need to retain one of the big six accounting firms, which I think there’s only four now, right? It’s the big four accounting firms now. But anyway, you’ve got to get these super, you know, name-on-the-building brand name accountants. It seems like when you make a decision like that, especially since presumably the buyer is drafting this contract, you’re really saying that, hey, seller, if you want to fix this, you’re going to go spend a lot of money to fight us on this thing. And they point out, and I’m sure this would be more now that we’re only going to resolve it if it’s $125,000 difference—they’ll resolve that either way, but we’re only going to pay for the accounting if there’s—you might have paid $125,000 for the accounting. What do you think about who bears the burden of redoing the math in this situation?

James Raanan Yeah, that’s a really excellent question that you kind of, you really intuited sort of the motivations here. Because here, by making the seller on the hook for the disputed items, you know, for paying, unless it gets to 125,000, which you can imagine, you know, I’m guessing that would have been a very big movement, It’s a significant disincentive for the seller to, you know, to really to go there, right? Now, as the seller’s counsel, you’re probably going to want to try and make it shared, because then, you know, then at least the buyer is on the hook and also has more skin in the game and is more likely to not play games. So in terms of the lack of gamesmanship, sharing it would be, you know, would be better, if I was seller’s counsel. So whoever was the buyer’s counsel, I think did a good job in this case, by disincentivizing the sellers to dispute.

Mike Whelan Yeah. Yeah. Bit of a poison pill in there. And then as we get to the money shot, right? I mean, this is literally the money shot, 2.8 talks about the post-closing purchase price adjustment. And this is a long section and I won’t read all of it, but it talks about the difference between the working capital target. The purchase price will be adjusted downward dollar for dollar basis. There’s stuff in here that, on the face of it, seems simple enough to calculate. But to your point, there’s a lot of accounting magic going on in the background. Do you think this section seals the deal? Do you think that it handles this question appropriately?

James Raanan I mean, I think that the problem is not so much with this section, because I think it is pretty clear. The issue is sort of within the definitions that underlie it. And it’s going back to what I was talking about in accounting principles, because it doesn’t go into any great detail about the accounting principles that we use in the preliminary closing balance sheet and the accounting principles used by…I mean, it does say that they have to be prepared in accordance with GAAP. But there may be other ways that the company was accounting for things that are different. So there may be something of a mismatch between how they’re calculating different things. So I think that’s an issue. I think some of the, like, some of the more simple things actually, such as the time frame, is an issue. So really the sellers only have ten business days to dispute. Otherwise this, you know, the money gets immediately paid out. Ten business days is not a long time. And typically you’re going to see 30 to 60 in more…let’s call them modern-day agreements. So I think that is, you know, that’s an issue. But I think that the, you know, the very laconic way in which it’s drafted, it works. And so, I don’t have an issue with that side of things. I think also, there are other nuances in here. For example, talks about the—you were talking before about the arbiter or Ernst & Young or a different accounting firm. So one of the issues they have is they say that if they don’t agree on Ernst &Young, then they have to jointly agree on another accountant. Whenever you have to agree to jointly agree, what if you don’t agree? And that allows somebody to play games and I think you’re much better off solving the whole mechanism through its end so that if somebody is playing games then there’s a default as to who you go to. But otherwise, it works.

Mike Whelan Yeah, it seems to me, as I’m stepping back to the bigger picture, to your point, this was a 1997 agreement and presumably the market has changed a bit. You know, right now is a pretty capital available market. ‘97, I believe, was a pretty capital available market. I was in my—just out of high school at the time, so I’m not entirely sure. But, you know, pretty capital intensive in the dot com era. And so I don’t know if the power structures have changed. What I’m seeing in this document, and correct me if I’m wrong, is is almost like a big brother, little brother kind of situation where the document is being used to kind of lead the buyer along—or the seller along—and get them into the deal where the big kids will handle things later and we’ll deal with all these these big questions that you don’t quite understand. Do you feel like the market has changed in that sense? Has the transparency in capital, has—literally, what the internet has done to make sellers much more informed? Has that improved these kinds of relationships? What have you seen change from 1997 to now in these kinds of agreements?

James Raanan You know, I think now they’re more balanced. I think seller’s council used to be, that you really felt that when you were the buyer’s counsel, everybody defaulted to the money. And I think now, and maybe it’s just because it’s, you know, my view is colored because of what’s happened over the last two or three years with such an availability of capital, has meant that money is chasing after deals. So you are seeing, you know, some of these mid positions that we were describing are being resolved either to the middle or even sometimes towards the seller’s counsel. You know, for example, in this deal, right, you have the money—a portion of money goes into escrow, which is fairly common—which is used here to both pay down any reconciliation in the purchase price or pay back, but also for some of the indemnifications. But I think that, you know, as I say, I think the main difference from this 1997 agreement to today is detail. But in terms of the concepts, it’s really very similar.

Mike Whelan And when you say detail, you mean this, however long this document is, this 35-page document is probably a 70-page document now, with all the iterations. And yeah, I love how contracts, you can always tell when you’re reading a contract, like, there was a story behind that section. You know, when there’s something that pops in there and you know, we’re going to share our drafts and you’re just like, why are there drafts? You know, there’s fun little contract clauses that come out. Well, I appreciate you bringing in one that brings us to foundational issues. I appreciate you sharing your perspective on it. James, for people who want to learn more about what you do and what you’re doing in Israel and your firm now, what’s the best way to reach out to you?

James Raanan So the best way is by email: James––j-a-m-e-s— at parnesraanan dot com—p-a-r-n-e-s-r-a-a-n-a-n dot com.

Mike Whelan Perfect. We’ll have that information available and this contract, as well and some other documents, over at Law Insider dot com slash resources. And for any of you that want to be our guest on this show and beat up contracts like we did with James, just email us. We’re at community at law insider dot com. Thank you again James. We’ll see you guys next time.